If you are a video service-provider today, what should your strategy be? This is a big question, and global professional services giant Accenture has recently attempted to address it in a report entitled The Digital Video Business.

Accenture’s answer is, in part, ‘it depends where you’re starting from’, but first, some statistics.

Looking at overall digital video industry performance from 2015 out to 2019, Accenture notes that OTT video delivery has been the ‘stand-out success’ of the video delivery sector, and has been responsible for “the vast majority of annual growth”: it estimates OTT CAGR from 2015 to 2019 at 15.6%, with broadcasters lagging behind at 2.9%, cable at 3.4% and telcos at 9.2% (see Figure 1).

Figure 1: Comparison of digital growth and traditional growth in pay-TV: Total pay-TV revenue, 2015-2019c, US$bn

| 2015 | 2016 | 2017 | 2018 | 2019 | CAGR (%) | |

| OTT | 23 | 27 | 31 | 36 | 42 | 15.6 |

| Telco | 36 | 40 | 44 | 48 | 51 | 9.2 |

| Cable | 94 | 97 | 101 | 104 | 108 | 3.4 |

| Broadcasting | 310 | 314 | 325 | 338 | 348 | 2.9 |

Source: PWC and SNL Kagan 2015

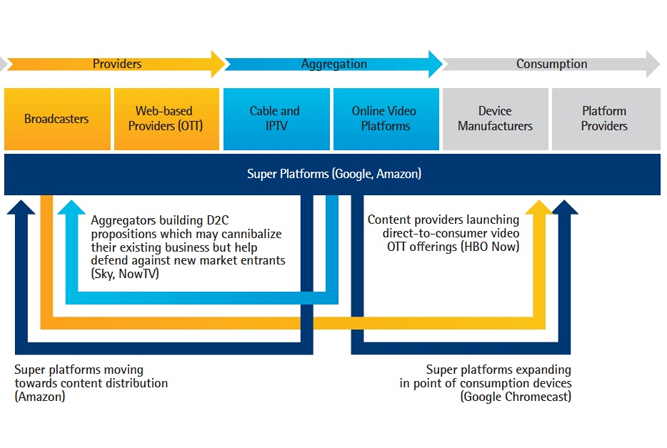

This OTT growth has been driven by a new type of company, Accenture says, characterised by new, agile market entrants with no legacy video business, investing in ‘webscale’ platforms and procuring premium content rights. The question is, how do you react if you’re one of the incumbents?

Here, Accenture distinguishes between ‘traditional content aggregators’ and ‘traditional content providers’:

- Traditional content aggregators “consolidate content from multiple providers and serve it to consumers”, providing them with a broader content proposition. They own the customer relationship, packaging and bundling content providers’ content, and collect subscriptions on the back of that. Traditional pay-TV operators fall into this category.

- Traditional content providers “typically own or acquire rights and monetize them across different distribution channels.” They manage content programming, curation, scheduling and linear distribution, while typically relying on aggregators for the consumer relationship on as many platforms as possible, and on ad revenues for monetisation. Traditional free-to-air broadcasters are a good example of this category.

Accenture argues that the OTT phenomenon has driven the creation of two new types of business, based on the two previous types.

- Digital Content Aggregators (DCAs) are typified by telcos such as BT, who now compete with traditional aggregators such as Sky and Virgin to provide triple-play (and in some cases quadruple-play) packages to their customers, delivering content to them through broadband networks rather than broadcast ones, based on a much smaller number of carriage deals.

- Digital Content Providers (DCPs), meanwhile, “aim to serve content they have acquired or produced across a wide array of different digital channels, including OTT and IP,” sometimes offering that content direct to consumers, and sometimes through collaborations with DCAs. Netflix is a high-profile example of a DCP, using OTT delivery with a D2C subscription model, but also being willing to tie up deals with aggregators (such as Virgin in the UK) for distribution within their bundles.

Accenture’s central argument is that, if you are a traditional content aggregator or content provider, you need to ‘pivot’ your organisation into either one or other of these two new business models – most likely, but not inevitably, with aggregators becoming DCAs and content providers becoming DCPs.

Accenture offers a number of industry examples where it believes such transformations are already taking place.

For Accenture, Sky represents an example of a traditional aggregator putting a foot in the DCP camp, with its Now TV service. This acquires rights (from its parent), and offers that content in D2C mode, acting in effect as a DCP.

Meanwhile, traditional aggregator US satellite operator Dish has taken the first steps towards adopting a DCA model with its Sling TV offering. This is a broadband-based bundle aimed at millenials and consumers without a pay-TV subscription, which has acquired around 500,000 subscribers in its first year.

At the same time, a number of traditional content providers in the US are evolving towards a DCP model through the launch of D2C standalone streaming services. Accenture points to the launches last year of HBO Now, Showtime’s OTT offering, and CBS All Access, as examples of this trend.

Accenture counsels that traditional content providers need to grow audience scale by working with as many traditional aggregators as possible, warning that “exclusive vertical integration with a single aggregator without global scale has rarely proved to be a winning strategy.” Here, the pressure to own the relationship with the consumer is driving many to explore D2C OTT moves, although Accenture describes these as “lateral rather than primary strategic moves.”

Meanwhile, for DCAs, “the growth of IP and OTT services has increased customer choice, meaning they now need to relate to two customers, their users and the DCPs they support.”

However they choose to ‘pivot’, Accenture points out that the process requires investment, in content, new capabilities and services, or through optimising distribution costs.

It believes that while some companies will test both DCA and DCP roles, “ultimately each must decide which type of business they intend to operate and start building for success now.”

Diagram at top from Accenture, showing value-chain shifts caused by OTT